[ad_1]

Final month, the Federal Reserve launched a brand new report: Financial Nicely-Being of U.S. Households in 2021 [PDF]. This annual survey gauges American monetary well being and attitudes. The 2021 version was carried out final November.

Listed here are some highlights from the report:

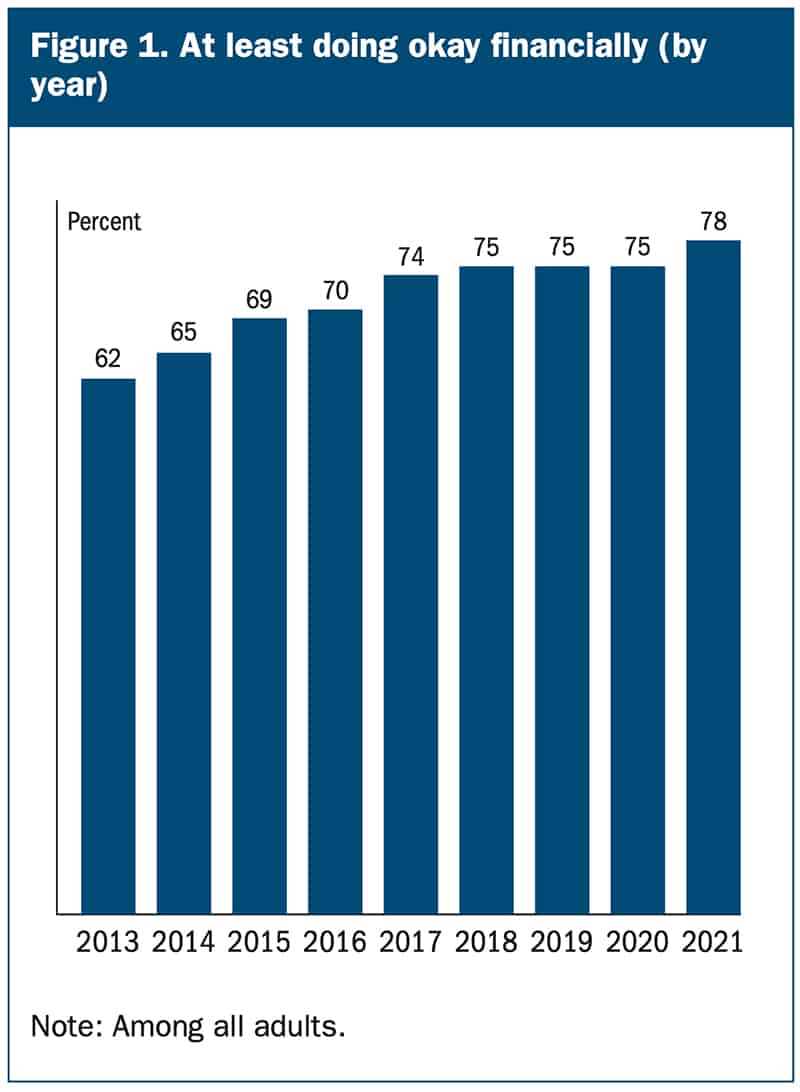

- Seventy-eight p.c of adults have been both doing okay or residing comfortably financially, the very best share with this degree of monetary well-being because the survey started in 2013.

- Fifteen p.c of adults with earnings lower than $50,000 struggled to pay their payments due to various month-to-month earnings.

- Fifteen p.c of staff stated they have been in a distinct job than twelve months earlier. Simply over six in ten individuals who modified jobs stated their new job was higher general, in contrast with one in ten who stated that it was worse.

- Sixty-eight p.c of adults stated they’d cowl a $400 emergency expense completely utilizing money or its equal, up from 50 p.c who would pay this manner when the survey started in 2013. (Be aware that this survey is the unique supply of this oft-quoted statistic.)

- Six p.c of adults didn’t have a checking account. Eleven p.c of adults with a checking account paid an overdraft charge within the earlier twelve months.

These little nuggets of information are fascinating, positive, however what I discover much more fascinating are the charts and graphs documenting long-term developments.

The Demographics of Financial Nicely-Being

Right here, as an illustration, is a chart that reveals how individuals really feel about their present monetary scenario:

In 2021, 78% of adults on this nation reported “doing okay” or “residing comfortably”. That is up considerably from when this survey began in 2013.

The following logical query, in fact, is how completely different demographics really feel about their monetary scenario. The Fed report provides some perception into that.

Here is a chart that reveals (as soon as once more) the worth of a faculty diploma).

Though it is common in some corners to bad-mouth faculty levels, in response to the U.S. Census Bureau (and many different sources) your schooling has a larger influence on lifetime incomes potential than some other demographic issue. Schooling issues greater than age. Schooling issues greater than race. Schooling issues greater than gender. In relation to earning profits, schooling issues most.

Subsequent, this is a chart from the Fed report that paperwork financial well-being by race and ethnicity:

Evidently financial well-being has improved throughout the board through the previous decade.

Private Nicely-Being Versus Nationwide Nicely-Being

To me, nonetheless, essentially the most fascinating chart is that this one, which compares respondents’ assessments of their private well-being with their evaluation of native and nationwide economies. Have a look at this chart and inform me what you make of it. (I’ve an opinion, however I would like you to develop your individual speculation earlier than studying mine…)

From the report:

Much like individuals’s perceptions of their native economic system, the share ranking the nationwide economic system favorably fell precipitously from 2019 to 2020, after the onset of the pandemic ). Nevertheless, individuals’s perceptions of the nationwide economic system continued to say no in 2021. Solely 24 p.c of adults rated the nationwide economic system as ‘good’ or ‘glorious’ in 2021, down 2 proportion factors from 2020 and about half the speed seen in 2019. This pattern contrasts starkly with individuals’s more and more favorable evaluation of their very own monetary well-being.

The Fed report tells us this discrepancy exists but it surely does not inform us why it exists. Why do 78% of Individuals say that their very own monetary scenario is a minimum of okay, however practically the identical quantity imagine that the nationwide economic system is not doing properly? I do not know. However I can consider two doable causes.

First, maybe most Individuals have realized to handle cash. Maybe they have been studying cash blogs and listening to cash podcasts, and now the teachings have sunk in. Possibly they’ve begun saving and investing correctly over the previous fifteen years in order that their private economic system is now shielded from the gyrations of the economic system at massive.

Maybe.

I harbor a suspicion, nonetheless, that there is one thing else at play right here.

Lengthy-time readers understand how a lot I abhor the information media. The mass media doesn’t report actuality. In case you envision life as a bell curve (or “regular distribution”, in the event you favor), the mass media tends to report solely outlier occasions — particularly adverse outlier occasions. The overwhelming majority of our lives comprise regular, optimistic, wholesome interactions and relationships and circumstances. The information does not report these.

On this case, I am unable to assist however ponder whether this disparity between perceptions of non-public financial well-being and nationwide financial well-being are pushed (a minimum of partly) by adverse financial information, information that highlights the issues with our economic system quite than the issues which are going proper.

That is what I suppose. What do you suppose? What is the cause for this hole in notion?

Last Ideas

There’s way more knowledge and perception on this 92-page report. I’ve highlighted just some stats from the primary part on general monetary well-being. Different sections cowl earnings, employment, sudden bills, banking and credit score, housing, schooling, pupil loans, retirement and investments, and extra.

I discovered the part on pupil loans fascinating too. It accommodates plenty of insights. Debtors with much less schooling, for instance, usually tend to be behind on mortgage funds. This makes some sense, I feel. In the meantime, fewer individuals are behind on funds than two years in the past (and this is applicable throughout all demographics).

Right here, although, is my favourite chart from the whole report. It measures the self-assessed worth of upper schooling:

Two issues appear clear right here. First, people who by no means needed to borrow for faculty imagine their schooling is price extra. Second, the extra schooling one obtains, the extra priceless it appears.

Okay, a 3rd factor. Examine this chart with the one I shared earlier that highlights monetary well-being by degree of schooling. It is clear that (objectively) schooling does enhance monetary well being. However those that have pupil loans cannot all the time see that. Their subjective expertise appears to contradict the information. Attention-grabbing…

Anyhow, the Fed’s Financial Nicely-Being of U.S. Households in 2021 is stuffed with fascinating information. It is price studying (or skimming) the following time you sit right down to waste time on the web!

[ad_2]

Source_link